These Non-Financial Benefits Turn a House into a Happy Home

There’s no denying the long-term financial benefits of owning a home, but today’s housing market may have you wondering if now’s still the time to buy. While the financial aspects of homeownership are important, the non-financial and emotional reasons are too. Here’s why. The word home truly means something different to everyone. Whether it’s sharing memories with loved ones around the kitchen table or settling in to read a book in your favorite chair, the emotional connections we have to our homes can be just as important as the financial ones. Here are some of the things that turn a house into a happy home. 1. You Can Be Proud of Your AccomplishmentBuying a home is a major life milestone. Whether you’re ready to buy your first home or your fifth, congratulations will be in order once you’ve achieved your goal. The sense of accomplishment you’ll feel at the end of your journey will truly make your home feel like your special place. Go ahead and smile – you’ve earned it. 2. You Have Your Own Designated Happy PlaceOwning your home offers not only safety and security, but also a comfortable place where you can relax and unwind after a long day. Sometimes that’s just what you need to feel refreshed and recharged. 3. You Can Find the Space To Meet Your NeedsWhether you want more room for your changing lifestyle (like a large backyard for entertaining or room for a home office) or you simply want to move closer to your loved ones, you can invest in a home that truly works for your evolving needs. 4. You Can Customize Your SurroundingsLooking to try one of those decorative wall treatments you saw online? Tired of paying an additional pet deposit for your apartment building? Or maybe you want to create an in-house yoga studio. You can do these things and much more when you own your home. Bottom LineWhether you’re planning to buy your first home, or you’re ready to move into a different one to meet your changing needs, think about the emotional benefits that can turn a house into a happy home. When you’re ready to make a move, let’s connect.  Get Ready To Buy a Home by Improving Your Credit Score

As the new year approaches, the idea of buying a home might be on your mind. It’s an exciting goal to set, and it's never too early to start laying the groundwork. One crucial step to prepare for homeownership is building a solid credit score. Lenders review your credit to assess your ability to make payments on time, pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from CNBC explains: “When it comes to mortgages, a higher credit score can save you thousands of dollars in the long run. This is because your credit score directly impacts your mortgage rate, which determines the amount of interest you’ll pay over the life of the loan.”This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today. According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. An article from Business Insider explains generally how your FICO score range can make an impact: “. . . you don’t need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you’re wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate. As FICO says: “While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

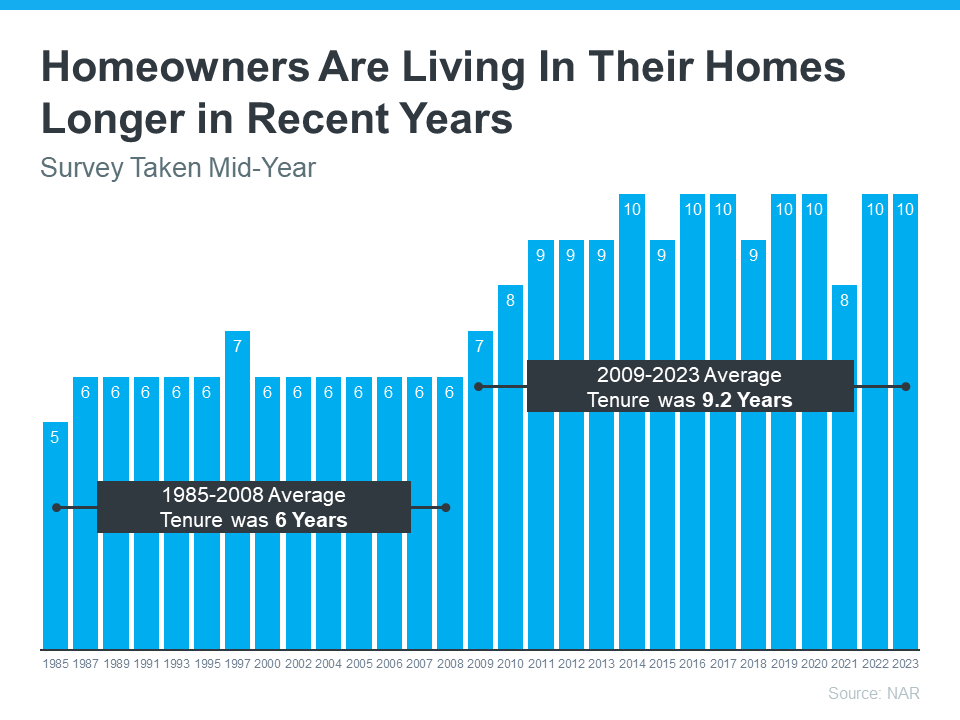

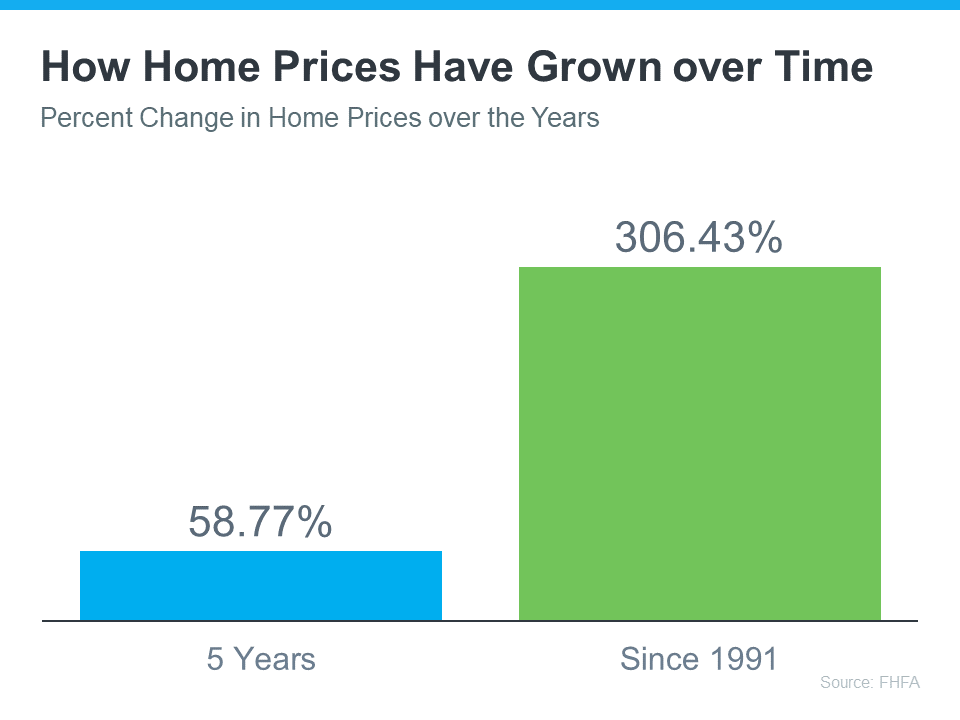

Bottom LineAs you set your sights on buying a home in the upcoming year, a focus on boosting your credit score could help you get a better mortgage rate when the time comes. If you want to learn more, connect with a trusted lender.  If you’re thinking about retirement or have already retired this year, it’s a good time to consider if your current house is still a good fit for the next chapter in your life. Fortunately, you may be in a better position to make a move than you realize. Here are a few things to think about as you decide whether or not to sell and make a move. How Long You’ve Been in Your Home From 1985 to 2008, the average length of time homeowners typically stayed in their homes was only six years. But according to the National Association of Realtors (NAR), that number is rising today, meaning many homeowners are living in their houses even longer (see graph below):  When you live in a home for a significant period of time, it’s natural for you to experience a number of changes in your life while you’re in that house. As those life changes and milestones happen, your needs may change. And if your current home no longer meets them, you may have better options waiting for you. How Much Equity You’ve Gained Additionally, if you’ve been in your house for more than a few years, you’ve likely built-up significant equity that can fuel your next move. That’s because the longer you’ve been in your house, the more likely it’s grown in value due to home price appreciation. Data from the Federal Housing Finance Agency (FHFA) illustrates that point (see graph below):  While home price growth varies by state and local area, the national average shows the typical homeowner who’s been in their house for five years saw it increase in value by nearly 60%. And the average homeowner who’s owned their home since 1991 saw it more than triple in value over that time. Consider Your Retirement Goals Whether you're looking to downsize, relocate to a dream destination, or simply be closer to loved ones, your home equity can be a key to realizing your homeownership goals. NAR shares that for recent home sellers, the primary reason to move was to be closer to loved ones. Whatever your home goals are, a trusted real estate agent can work with you to find the best option. They’ll help you sell your current house and guide you through buying the home that’s right for your lifestyle today.. Bottom Line Retirement can bring about major changes in your life, including what you need from your home. Let’s connect to explore the available homes in our area.  What You Need To Know About Saving for a Home in 2024

If you’re planning to buy a home, knowing what to budget for and how to save may sound intimidating – but it doesn’t have to be. One way to ease those concerns is to make sure you understand some of the costs you may encounter up front. And to do that, always turn to trusted real estate professionals. They can help you set a plan and take a strategic look at your budget and your process before you even get started. Here are just a few things experts say you should be thinking about. 1. Down PaymentSaving for your down payment is likely top of mind as you set out to buy a home. But do you know how much you’ll need? While every buyer’s situation is different, there’s a common misconception that putting 20% of the purchase price down is required. An article from the Mortgage Reports explains why that’s not always the case: “The idea that you have to put 20% down on a house is a myth. . . . The right amount depends on your current savings and your home buying goals.”To understand your options, partner with trusted real estate professionals to go over the various loan types, down payment assistance programs, and what each one requires. The more you know ahead of time, the easier the process will be. 2. Closing CostsMake sure you also budget for closing costs, which are a collection of fees and payments made to the various parties involved in your transaction. Bankrate explains: “Closing costs are the fees you pay when finalizing a real estate transaction, whether you’re refinancing a mortgage or buying a new home. These costs can amount to 2 to 5 percent of the mortgage so it’s important to be financially prepared for this expense.”The best way to understand what you’ll need at the closing table is to work with a trusted lender. They can provide you with answers to the questions you might have. 3. Earnest Money DepositIf you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). An EMD is money you pay as a show of good faith when you make an offer on a house. According to Realtor.com, it’s usually between 1% and 2% of the total home price. This deposit works like a credit. It’s not an added expense – it’s paying a portion of your costs upfront. You’re using some of the money you’ve already saved for your purchase to show the seller you’re committed and serious about buying their house. Realtor.com describes how it works as part of your sale: “It tells the real estate seller you’re in earnest as a buyer . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”Keep in mind, an EMD isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your local area. They’ll advise you on what moves you should make so you can make the best possible decisions throughout the buying process. Bottom LineWhen buying a home, being informed about what to save for is key. Let’s connect so you’ll have an expert on your side to answer any questions you have along the way.  3 Keys To Hitting Your Homeownership Goals in 2024

If buying or selling a home is your goal for 2024, it’s important to understand today’s housing market, know your why, and work with industry experts to bring your homeownership vision for the new year into focus. Over the last year, the economy had a big impact on the housing market, and likely on your wallet too. That’s why it’s critical to have a clear picture of not just the market today, but also on what you want out of it when you buy or sell a home. Danielle Hale, Chief Economist at Realtor.com, explains: “The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, so that you can stay in your home long enough that buying is a sound financial decision.”Here are a few things to think through as you define your goals for 2024. 1. Know Your WhyYou’re dreaming about making a move for a reason – what is it? No matter what’s happening in the market, there are still many compelling reasons to buy a home today. Your needs may have changed in a way your current house can’t address, or you could be ready to step into homeownership for the first time. Use your why and your motivation as a guidepost in partnership with an expert advisor to make sure your move gives you a lasting sense of accomplishment. 2. Figure Out What Your Next Home Needs To Look LikeYou know you want to move, but how would you describe your dream home? The number of homes for sale has grown recently, and that could mean more options to choose from when you buy. But overall housing supply is still lower than more normal years in the market, so you’ll have to work closely with a pro to find what you’re looking for. Just be sure to keep your budget in mind as you balance your wants and needs. The better you understand what’s essential and where you can be flexible, the easier it will be to find a home that’s right for you. 3. Determine if You’re Ready To BuyGetting clear on your budget and available savings is essential before you get too far into the process. Partnering with a local agent and a lender early is the best way to make sure you’re in a good position to buy. This could include planning how much to save for a down payment, getting pre-approved for a home loan, and assessing your current home equity if you’re selling your existing house. A Professional Will Guide You Through Every Step of the ProcessBuying or selling a home takes expertise to navigate. If that feels a bit overwhelming, that’s normal. Don’t let uncertainty hold you back from your goals this year. A trusted expert will help you bridge that gap and give you the facts and advice you need about today’s housing market. Bottom LineLet’s connect to plan how to make your homeownership dreams a reality in 2024.  Things To Consider If Your House Didn’t Sell

If your listing has expired and your house didn’t sell, it's completely normal to feel a mix of frustration and disappointment. Understandably, you're probably wondering what may have gone wrong. Here are three questions to think about as you figure out what to do next. Did You Limit Access to Your House?One of the biggest mistakes you can make when selling your house is restricting the days and times when potential buyers can tour it. Being flexible with your schedule is important, even though it might feel a bit stressful to drop everything and leave when buyers want to see it. After all, minimal access means minimal exposure to buyers. ShowingTime advises: “. . . do your best to be as flexible as possible when granting access to your house for showings.”Sometimes, the most determined buyers might come from far away. Since they’re traveling to see your house, they may not be able to change their plans easily if you only offer limited times for showings. So, try to make your house available as much as you can to accommodate them. It's simple – if no one’s able to look at it, how will it sell? Did You Make Your House Stand Out?When you're selling your house, the old saying matters: you never get a second chance to make a first impression. Putting in the work to make the exterior of your home look nice is just as important as how you stage it inside. Freshen up your landscaping to boost your home’s curb appeal so you can make an impact upfront. As an article from U.S. News says: “After all, if people drive by, but aren’t interested enough to walk through the front door, you’ll never sell your house.”But don’t let that impact stop at the front door. By removing personal items and reducing clutter inside, you give buyers more freedom to picture themselves in the home. Plus, a fresh coat of paint or thorough floor cleaning can work wonders in sprucing up the house for potential buyers. Did You Price Your House at Market Value?Setting the right price is key. While it might be tempting to push the price higher to maximize your profit, overpricing your house can actually turn off potential buyers and slow down the selling process. Forbes notes: “Pricing a home too high could lead to a slower sale or force the seller to drop their price.”If your house is priced higher than others like it, it may discourage buyers, resulting in increased time on the market. Pay attention to the feedback people give your agent during open houses and showings. If lots of people are saying the same thing, it might be a good idea to think about lowering the price. For all these insights and more, rely on a trusted real estate agent. A great agent will offer expert advice on relisting your house with effective strategies to get it sold. Bottom LineIt’s natural to feel disappointed when your listing has expired and your house didn’t sell. Let’s connect to determine what happened, and what changes you should make to get your house back on the market. |

Let's ConnectWith the correct person by your side, the buying and selling process doesn't have to be full of stress, doubt and anxiety - it can actually be FUN! Archives

July 2024

Categories

All

Jacquelyn Duke, Realtor®

Licensed to Sell in the State of Iowa [email protected] (515) 240-7483 Realty One Group Impact 617 SW 3rd Street Ste 101 Ankeny, IA 50023 Disclaimer: The material on this site is solely for informational purposes. No warranties or representations have been made.

|

RSS Feed

RSS Feed