Don’t Fall for the Next Shocking Headlines About Home Prices

If you’re thinking of buying or selling a home, one of the biggest questions you have right now is probably: what’s happening with home prices? And it’s no surprise you don’t have the clarity you need on that topic. Part of the issue is how headlines are talking about prices. They’re basing their negative news by comparing current stats to the last few years. But you can’t compare this year to the ‘unicorn’ years (when home prices reached record highs that were unsustainable). And as prices begin to normalize now, they’re talking about it like it’s a bad thing and making people fear what’s next. But the worst home price declines are already behind us. What we’re starting to see now is the return to more normal home price appreciation. To help make home price trends easier to understand, let’s focus on what’s typical for the market and omit the last few years since they were anomalies. Let’s start by talking about seasonality in real estate. In the housing market, there are predictable ebbs and flows that happen each year. Spring is the peak homebuying season when the market is most active. That activity is typically still strong in the summer but begins to wane as the cooler months approach. Home prices follow along with seasonality because prices appreciate most when something is in high demand. That’s why, before the abnormal years we just experienced, there was a reliable long-term home price trend. The graph below uses data from Case-Shiller to show typical monthly home price movement from 1973 through 2021 (not adjusted, so you can see the seasonality): As the data from the last 48 years shows, at the beginning of the year, home prices grow, but not as much as they do entering the spring and summer markets. That’s because the market is less active in January and February since fewer people move in the cooler months. As the market transitions into the peak homebuying season in the spring, activity ramps up, and home prices go up a lot more in response. Then, as fall and winter approach, activity eases again. Price growth slows, but still typically appreciates. Why This Is So Important to UnderstandIn the coming months, as the housing market moves further into a more predictable seasonal rhythm, you’re going to see even more headlines that either get what’s happening with home prices wrong or, at the very least, are misleading. Those headlines might use a number of price terms, like:

Bottom LineIf you have questions about what’s happening with home prices in our local area, let’s connect.

0 Comments

Tips for Making Your Best Offer on a Home

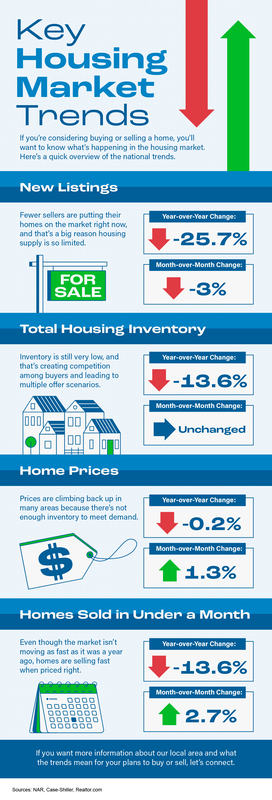

While the wild ride that was the ‘unicorn’ years of housing is behind us, today’s market is still competitive in many areas because the supply of homes for sale is still low. If you’re looking to buy a home this season, know that the peak frenzy of bidding wars is in the rearview mirror, but you may still come up against some multiple-offer scenarios. Here are a few things to consider to help you put your best foot forward when making an offer on a home. 1. Lean on a Real Estate ProfessionalRely on an agent who can support your goals and help you understand what’s happening in today’s housing market. Agents are experts in the local market and on the national trends too. They’ll use both of those areas of expertise to make sure you have all the information you need to move with confidence. Plus, they know what’s worked for other buyers in your area and what sellers may be looking for in an offer. It may seem simple, but catering to what a seller needs can help your offer stand out. As an article from Forbes says: "Getting to know a local realtor where you’re hoping to buy can also potentially give you a crucial edge in a tight housing market." 2. Get Pre-Approved for a Home LoanHaving a clear budget in mind is especially important right now given the current affordability challenges. The best way to get a clear picture of what you can borrow is to work with a lender so you can get pre-approved for a home loan. That’ll help you be more financially confident because you’ll have a better understanding of your numbers. It shows sellers you’re serious, too. And that can give you a competitive edge if you do get into a multiple-offer scenario. 3. Make a Fair OfferIt’s only natural to want the best deal you can get on a home. However, submitting an offer that’s too low does have some risks. You don’t want to make an offer that will be tossed out as soon as it’s received just to see if it sticks. As Realtor.com explains: “. . . an offer price that’s significantly lower than the listing price, is often rejected by sellers who feel insulted . . . Most listing agents try to get their sellers to at least enter negotiations with buyers, to counteroffer with a number a little closer to the list price. However, if a seller is offended by a buyer or isn’t taking the buyer seriously, there’s not much you, or the real estate agent, can do.”The expertise your agent brings to this part of the process will help you stay competitive and find a price that’s fair to you and the seller. 4. Trust Your Agent’s Expertise Throughout NegotiationsDuring the ‘unicorn’ years of housing, some buyers skipped home inspections or didn’t ask for concessions from the seller in order to submit the winning bid on a home. An article from Bankrate explains this isn’t happening as often today, and that’s good news: “While the market has largely calmed down since then, sellers are still very much in the driver’s seat in this era of scarce housing inventory. It’s not as common for buyers to waive inspections anymore, but it does still happen. . . . It’s in the buyer’s best interest to have a home inspected . . . Inspections alert you to existing or potential problems with the home, giving you not just an early heads up but also a useful negotiating tactic.”Fortunately, today’s market is different, and you may have more negotiating power than before. When putting together an offer, your trusted real estate advisor will help you think through what levers to pull and which ones you may not want to compromise on. Bottom LineWhen you buy a home this summer, let’s connect so you have an expert on your side who can help you make your best offer.  Key Housing Market Trends [INFOGRAPHIC] Some Highlights

Pricing Your House Right Still Matters Today

While this isn’t the frenzied market we saw during the ‘unicorn’ years, homes that are priced right are still selling quickly and seeing multiple offers right now. That’s because the number of homes for sale is still so low. Data from the National Association of Realtors (NAR) shows 76% of homes sold within a month and the average saw 3.5 offers in June. To set yourself up to see advantages like these, you need to rely on an agent. Only an agent has the expertise needed to find the right asking price for your house. Here’s what’s at stake if that price isn’t accurate for today’s market value. The price you set for your house sends a message to potential buyers.Price it too low and you might raise questions about your home’s condition or lead buyers to assume something is wrong with it. Not to mention, if you undervalue your house, you could leave money on the table, which decreases your future buying power. On the other hand, price it too high and you run the risk of deterring buyers from ever touring it in the first place. When that happens, you may have to do a price drop to try to re-ignite interest in your house when it sits on the market for a while. But be aware that a price drop can be seen as a red flag for some buyers who will wonder why the price was reduced and what that means about the home. A recent article from NerdWallet sums it up like this: "Your house’s market debut is your first chance to attract a buyer and it’s important to get the pricing right. If your home is overpriced, you run the risk of buyers not seeing the listing . . . But price your house too low and you could end up leaving some serious money on the table. A bargain-basement price could also turn some buyers away, as they may wonder if there are any underlying problems with the house."Think of pricing your home as a target. Your goal is to aim directly for the center – not too high, not too low, but right at market value. Pricing your house fairly based on market conditions increases the chance you’ll have more buyers who are interested in purchasing it. That makes it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly. To get a high-level look into the potential downsides of over or underpricing your house and the perks that come with pricing it at market value, see the chart below: Lean on a Professional’s Expertise to Price Your House RightSo why is an agent essential in finding the right price? Your local agent has the skill and the insight necessary to find the market value of your home. They’ll use their expertise to determine a realistic listing price by assessing:

Sellers: Don’t Let These Two Things Hold You Back

Many homeowners thinking about selling have two key things holding them back. That’s feeling locked in by today’s higher mortgage rates and worrying they won’t be able to find something to buy while supply is so low. Let’s dive into each challenge and give you some helpful advice on how to overcome these obstacles. Challenge #1: The Reluctance to Take on a Higher Mortgage RateAccording to the Federal Housing Finance Agency (FHFA), the average interest rate for current homeowners with mortgages is less than 4% (see graph below): But today, the typical 30-year fixed mortgage rate offered to buyers is closer to 7%. As a result, many homeowners are opting to stay put instead of moving to another home with a higher borrowing cost. This is a situation known as the mortgage rate lock-in effect. The Advice: Waiting May Not Pay OffWhile experts project mortgage rates will gradually fall this year as inflation cools, that doesn’t necessarily mean you should wait to sell. Mortgage rates are notoriously hard to predict. And, right now home prices are back on the rise. If you move now, you’ll at least beat rising home prices when you buy your next home. And, if experts are right and rates fall, you can always refinance later if that happens. Challenge #2: The Fear of Not Finding Something to BuyWhen so many homeowners are reluctant to take on a higher rate, fewer homes are going to come onto the market. That’s going to keep inventory low. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains: “Inventory will remain tight in the coming months and even for the next couple of years. Some homeowners are unwilling to trade up or trade down after locking in historically-low mortgage rates in recent years.”Even though you know this limited housing supply helps your house stand out to eager buyers, it may also make you feel hesitant to sell because you don’t want to struggle to find something to purchase. The Advice: Broaden Your SearchIf fear you won’t be able to find your next home is the primary thing holding you back, remember to consider all your options. Looking at all housing types including condos, townhouses, and even newly built homes can help give you more to choose from. Plus, if you’re able to work fully remote or hybrid, you may be able to consider areas you hadn’t previously searched. If you can look further from your place of work, you may have more affordable options. Bottom LineInstead of focusing on the challenges, focus on what you can control. Let’s connect so you’re working with a professional who has the experience to navigate these waters and find the perfect home for you.  How To Know If You’re Ready to Buy a Home

If you’re trying to decide if you’re ready to buy a home, there’s probably a lot on your mind. You’re thinking about your finances, today’s mortgage rates and home prices, the limited supply of homes for sale, and more. And, you’re juggling how all of those things will impact the choice you’ll make. While housing market conditions are definitely a factor in your decision, your own life and your finances may be even more important. As an article from NerdWallet says: “Housing market trends give important context. But whether this is a good time to buy a house also depends on your financial situation, life goals and readiness to become a homeowner.”Instead of trying to time the market, it may help to focus on what you can control. Here are a few questions that can give you clarity on whether you’re ready to make your move. 1. Do You Have a Stable Job?One thing to consider is how stable you feel your employment is. Buying a home is a big purchase, and you’re going to sign a home loan stating you’re going to pay that loan back. That can feel like a big obligation. Knowing you have a reliable job and income coming in can help put your mind at ease. As NerdWallet explains: “A mortgage is a big commitment . . . Wait until your employment is stable before thinking about buying a house.” 2. Have You Figured Out What You Can Afford?To make sure you have a good idea of what you’ll need to save and what you can expect to spend on your monthly payment, talk to a trusted lender. They’ll be able to tell you about the pre-approval process and what you can borrow, current mortgage rates and approximate monthly payments, closing costs to anticipate, what percent of the purchase price of the home you’ll need for a down payment, and more. The best part is you may find out you’re closer to your goals than you realized. You don’t necessarily need to put 20% down, unless it’s specified by your lender or loan type. As Down Payment Resource says: “A 20% down payment on a home is great, but . . . Many mortgages require no more than 3% to 5% of the purchase price as a down payment. Plus, there are loans and grants that may help cover these costs. Search for down payment assistance in your area, and discuss your results with your mortgage lender . . .” 3. How Long Do You Plan to Live There?Another important thing to think about is how long you plan to stay put. It takes time to build equity in your home through paying down your loan and home price appreciation. If you plan to move too soon, you may not recoup your investment. For example, if you’re looking to sell and move again in a year, it might not make sense to buy right now. As a recent article from CNET says: “Buying a home is a good idea if you’re planning to stay put for at least three years. Home values typically increase between 2% and 5% annually, so you could end up paying more in closing costs than you’d earn in proceeds if you sell after only a year or two.”So, think about your future. If you plan to transfer to a new city with the upcoming promotion you’re working toward or you anticipate your loved ones will need you to move closer to take care of them, that’s something to factor in. Above all else, the most important question to answer is: do you have a team of real estate professionals in place? If not, finding a trusted local agent and a lender is a good first step. Bottom LineIf you’re trying to decide if you’re ready to buy a home, these questions can help. But ultimately, your best and more reliable resource is the help of trusted real estate professionals.  How Inflation Affects Mortgage Rates

When you read about the housing market in the news, you might see something about a recent decision made by the Federal Reserve (the Fed). But how does this decision affect you and your plans to buy a home? Here's what you need to know. The Fed is trying hard to reduce inflation. And even though there’s been 12 straight months where inflation has cooled (see graph below), the most recent data shows it’s still higher than the Fed’s target of 2%: While you may have been hoping the Fed would stop their hikes since they’re making progress on their goal of bringing down inflation, they don’t want to stop too soon, and risk inflation climbing back up as a result. Because of this, the Fed decided to increase the Federal Funds Rate again last week. As Jerome Powell, Chairman of the Fed, says: “We remain committed to bringing inflation back to our 2 percent goal and to keeping longer-term inflation expectations well anchored.”Greg McBride, Senior VP, and Chief Financial Analyst at Bankrate, explains how high inflation and a strong economy play into the Fed’s recent decision: “Inflation remains stubbornly high. The economy has been remarkably resilient, the labor market is still robust, but that may be contributing to the stubbornly high inflation. So, Fed has to pump the brakes a bit more.”Even though a Federal Fund Rate hike by the Fed doesn’t directly dictate what happens with mortgage rates, it does have an impact. As a recent article from Fortune says: “The federal funds rate is an interest rate that banks charge other banks when they lend one another money . . . When inflation is running high, the Fed will increase rates to increase the cost of borrowing and slow down the economy. When it’s too low, they’ll lower rates to stimulate the economy and get things moving again.” How All of This Affects You In the simplest sense, when inflation is high, mortgage rates are also high. But, if the Fed succeeds in bringing down inflation, it could ultimately lead to lower mortgage rates, making it more affordable for you to buy a home. This graph helps illustrate that point by showing that when inflation decreases, mortgage rates typically go down, too (see graph below): As the data above shows, inflation (shown in the blue trend line) is slowly coming down and, based on historical trends, mortgage rates (shown in the green trend line) are likely to follow. McBride says this about the future of mortgage rates: “With the backdrop of easing inflation pressures, we should see more consistent declines in mortgage rates as the year progresses, particularly if the economy and labor market slow noticeably.”Bottom LineWhat happens to mortgage rates depends on inflation. If inflation cools down, mortgage rates should go down too. Let's talk so you can get expert advice on housing market changes and what they mean for you. |

Let's ConnectWith the correct person by your side, the buying and selling process doesn't have to be full of stress, doubt and anxiety - it can actually be FUN! Archives

July 2024

Categories

All

Jacquelyn Duke, Realtor®

Licensed to Sell in the State of Iowa [email protected] (515) 240-7483 Realty One Group Impact 617 SW 3rd Street Ste 101 Ankeny, IA 50023 Disclaimer: The material on this site is solely for informational purposes. No warranties or representations have been made.

|

RSS Feed

RSS Feed