Over the past year or so, a lot of people have been talking about how tough it is to buy a home. And while there’s no arguing affordability is still tight, there are signs it’s starting to get a bit better and may improve even more throughout the year. Elijah de la Campa, Senior Economist at Redfin, says: “We’re slowly climbing our way out of an affordability hole, but we have a long way to go. Rates have come down from their peak and are expected to fall again by the end of the year, which should make homebuying a little more affordable and incentivize buyers to come off the sidelines.”Here’s a look at the latest data for the three biggest factors that affect home affordability: mortgage rates, home prices, and wages. 1. Mortgage RatesMortgage rates have been volatile this year – bouncing around in the upper 6% to low 7% range. That’s still quite a bit higher than where they were a couple of years ago. But there is a sliver of good news. Despite the recent volatility, rates are still lower than they were last fall when they reached nearly 8%. On top of that, most experts still think they’ll come down some over the course of the year. A recent article from Bright MLS explains: “Expect rates to come down in the second half of 2024 but remain above 6% this year. Even a modest drop in rates will bring both more buyers and more sellers into the market.” Any drop in rates can make a difference for you. When rates go down, you can afford the home you really want more easily because your monthly payment would be lower. 2. Home PricesThe second big factor to think about is home prices. Most experts project they'll keep going up this year, but at a more normal pace. That’s because there are more homes on the market this year, but still not enough for everyone who wants to buy one. The graph below shows the latest 2024 home price forecasts from seven different organizations:  These forecasts are actually good news for you because it means the prices aren't likely to shoot up sky high like they did during the pandemic. That doesn’t mean they’re going to fall – they'll just rise at a slower pace. 3. WagesOne factor helping affordability right now is the fact that wages are rising. The graph below uses data from the Federal Reserve to show how wages have been growing over time:  Check out the blue dotted line. That shows how wages typically rise. If you look at the right side of the graph, you'll see wages are climbing even faster than normal right now.

Here’s how this helps you. If your income has increased, it's easier to afford a home because you don't have to spend as big of a percentage of your paycheck on your monthly mortgage payment. Bottom LineIf you stack these factors up, you’ll see mortgage rates are still projected to come down a bit later this year, home prices are going up at a more moderate pace, and wages are growing quicker than normal. Those trends are a good sign for your ability to afford a home.  If you’re thinking about buying a home, chances are you’ve got mortgage rates on your mind. You’ve heard about how they impact how much you can afford in your monthly mortgage payment, and you want to make sure you’re factoring that in as you plan your move. The problem is, with all the headlines in the news about rates lately, it can be a bit overwhelming to sort through. Here’s a quick rundown of what you really need to know. The Latest on Mortgage RatesRates have been volatile – that means they’re bouncing around a bit. And, you may be wondering, why? The answer is complicated because rates are affected by so many factors. Things like what’s happening in the broader economy and the job market, the current inflation rate, decisions made by the Federal Reserve, and a whole lot more have an impact. Lately, all of those factors have come into play, and it’s caused the volatility we’ve seen. As Odeta Kushi, Deputy Chief Economist at First American, explains: “Ongoing inflation deceleration, a slowing economy and even geopolitical uncertainty can contribute to lower mortgage rates. On the other hand, data that signals upside risk to inflation may result in higher rates.” Professionals Can Help Make Sense of it AllWhile you could drill down into each of those things to really understand how they impact mortgage rates, that would be a lot of work. And when you’re already busy planning a move, taking on that much reading and research may feel a little overwhelming. Instead of spending your time on that, lean on the pros. They coach people through market conditions all the time. They’ll focus on giving you a quick summary of any broader trends up or down, what experts say lies ahead, and how all of that impacts you. Take this chart as an example. It gives you an idea of how mortgage rates impact your monthly payment when you buy a home. Imagine being able to make a payment between $2,500 and $2,600 work for your budget (principal and interest only). The green part in the chart shows payments in that range or lower based on varying mortgage rates (see chart below):  As you can see, even a small shift in rates can impact the loan amount you can afford if you want to stay within that target budget.

It’s tools and visuals like these that take everything that’s happening and show what it actually means for you. And only a pro has the knowledge and expertise needed to guide you through them. You don’t need to be an expert on real estate or mortgage rates, you just need to have someone who is, by your side. Bottom LineHave questions about what’s going on in the housing market? Let’s connect so we can take what’s happening right now and figure out what it really means for you.  If you’ve been keeping up with the news lately, you’ve probably come across some articles saying the number of foreclosures in today’s housing market is going up. And that may leave you feeling a bit worried about what’s ahead, especially if you owned a home during the housing crash in 2008. The reality is, while increasing, the data shows a foreclosure crisis is not where the market is headed. Here’s the latest information stacked against the historical data to put your mind at ease. The Headlines Make the Increase Sound Dramatic – But It’s NotThe increase the media is calling attention to is a little bit misleading. That’s because it’s comparing the most recent numbers to a time when foreclosures were at historic lows. And that lopsided comparison is making it sound like a much bigger deal than it actually is. Back in 2020 and 2021, there was a moratorium and forbearance program that helped millions of homeowners avoid foreclosure during challenging times. That’s why numbers for just a few years ago were so low. Now that the moratorium has come to an end, foreclosures are resuming and that means numbers are rising. But it’s an expected increase, not a surprise, and not a cause for alarm. Just because foreclosure filings are up doesn’t mean the housing market is in trouble. To prove that to you, let’s expand the comparison out a bit more. Specifically, we’ll go all the way back to the housing crash in 2008 – since that’s what people worry may happen again. The graph below uses research from ATTOM, a property data provider, to show foreclosure activity has been consistently lower since the crash in 2008:  What the data shows is that things now aren’t anything like they were surrounding the housing crash. The bars in red are when there were over 1 million foreclosure filings a year. In 2023, there were roughly 357,000. That’s a big difference.

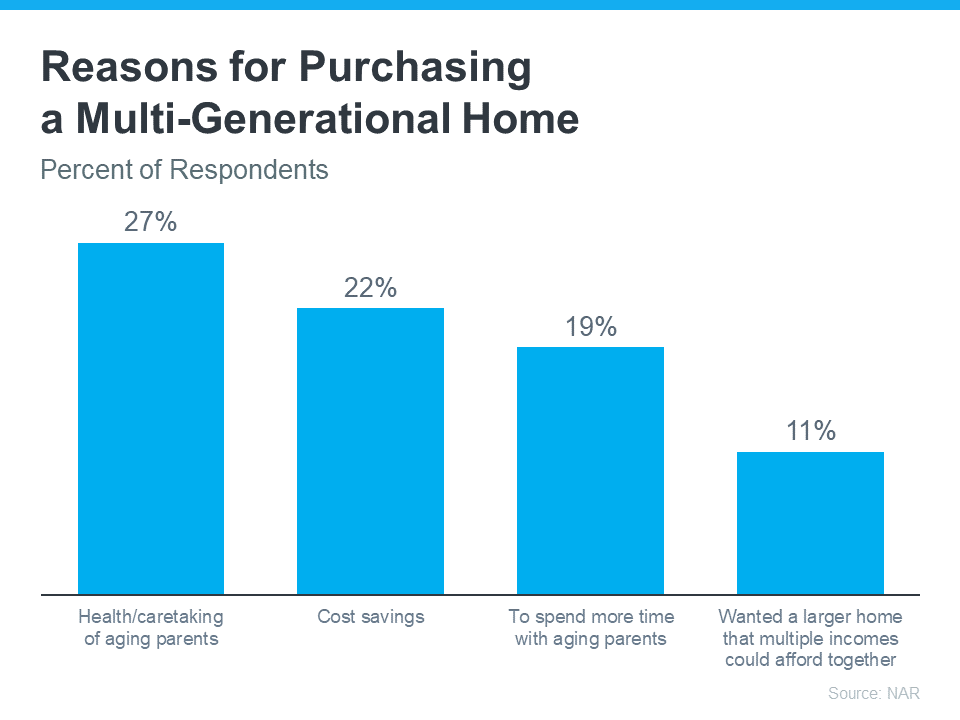

A recent article from Bankrate explains one of the reasons things aren’t like they were back then: “In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.”Basically, foreclosure activity is nothing like it was during the crash. That’s because most homeowners today have enough equity to keep them from going into foreclosure. And that’s a really good thing for homeowners and for the market. The reality is, the data shows a foreclosure crisis is not where the market is today, or where it’s headed. Bottom LineRight now, putting the data into context is more important than ever. While the housing market is experiencing an expected rise in foreclosures, it’s nowhere near the crisis levels seen when the housing bubble burst, and that won’t lead to a crash in home prices.  Ever thought about living in the same house with your grandparents, parents, or other loved ones? You're not alone. A lot of people are choosing to buy multi-generational homes where everyone can live together. Let's check out why they think it’s a good idea to see if it might be a good fit for you, too. Why People Are Choosing Multi-Generational LivingAccording to the National Association of Realtors (NAR), here are just a few key reasons buyers opted for multi-generational homes over the past year (see graph below):  Two of the top reasons had to do with aging parents. 27% of buyers chose multi-generational homes so they could take care of their parents more easily. And 19% did it to spend more time with them. A lot of older adults want to age in place, and living in a home with loved ones can help them do just that. If your parents are hoping to do the same, but need a bit of help, a multi-generational home may be worth considering.

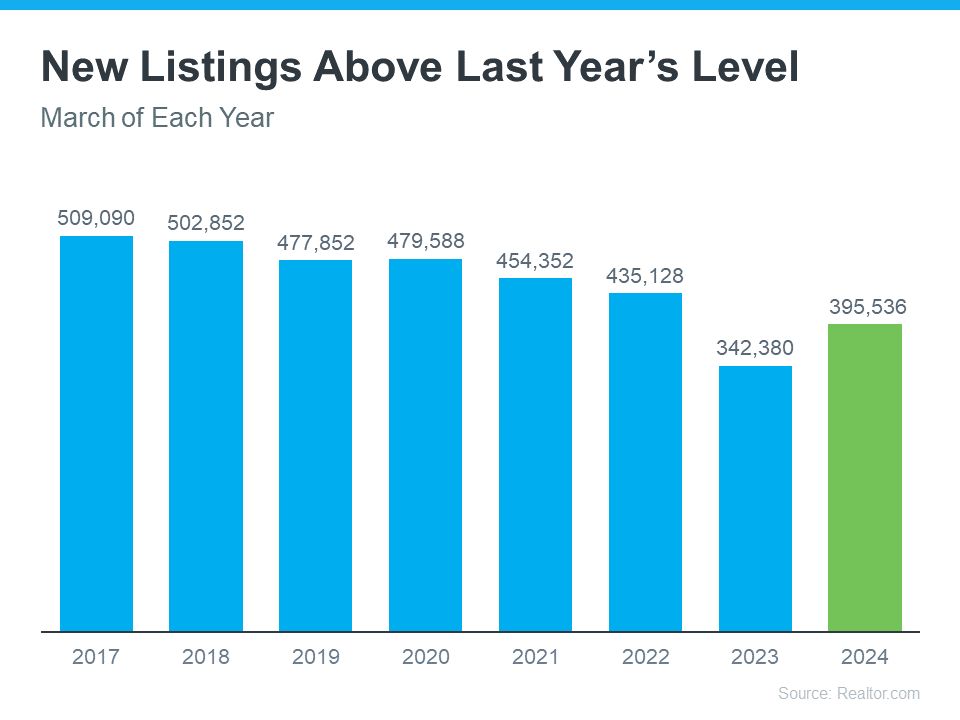

But buying a multi-generational home isn’t just about being close or taking care of the people you love—it can save you money, too. 22% of buyers say they picked a multi-generational home to cut down on costs, and 11% needed a bigger house multiple incomes could afford together. Sharing costs like the mortgage and utilities can make owning a home more affordable. This is especially helpful for first-time homebuyers who might find it challenging to buy a place on their own in today's market. As Axios explains: “Financial concerns and caregiving needs are two of the major reasons people live with their parents (and parents’ parents).” How an Agent Is Key in Finding the Right Home for YouLooking for the perfect multi-generational home is a bit trickier than finding a regular house. You've got more people, which means more opinions and needs to think about. It's kind of like putting together a puzzle where all the pieces need to fit perfectly. If you're into the idea of living with loved ones and want all the benefits that come with it, team up with a local real estate agent who can help you out. Bottom LineWhether you're looking to save money or want to take care of your loved ones, buying a multi-generational home might be a good idea for you. If you want to find out more, let’s talk.  The number of homes for sale is playing a big role in today’s housing market. And, if you’re considering whether or not to list your house, today’s limited supply is one of the biggest advantages you have right now. That’s because your house stands out more when the inventory is low, especially if it’s priced right. But the supply of homes for sale is growing. According to the latest data from Realtor.com, new listings (homeowners who just put their house up for sale) are trending up (see graph below):  This graph shows more homeowners are putting that sale sign up in their yards compared to the same time last year. As Realtor.com says:

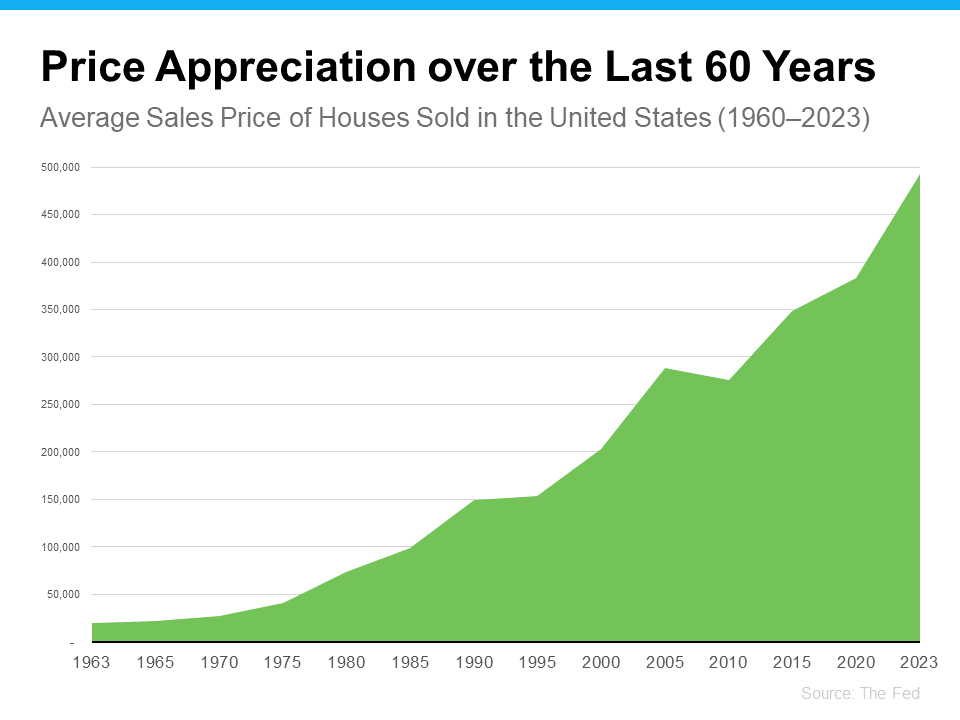

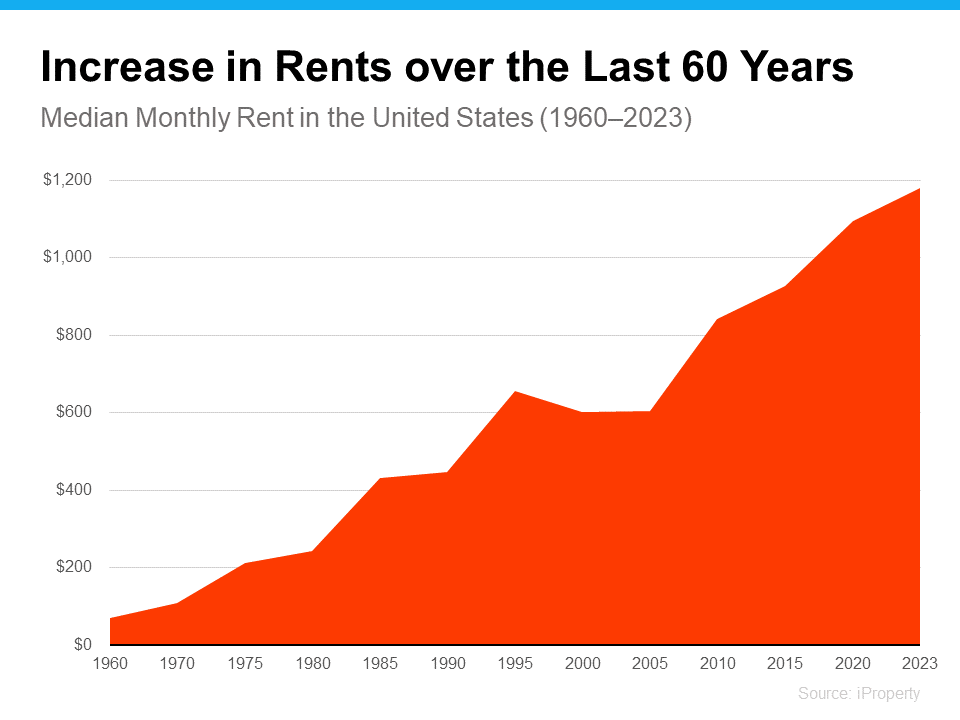

“. . . sellers turned out in higher numbers this March as newly listed homes were 15.5% above last year’s levels. This marked the fifth month of increasing listing activity after a 17-month streak of decline.” What This Means for YouIf you’ve been putting off selling your house, maybe it’s time to start thinking about it again – before your neighbors do. While we’re not going to suddenly have a surplus of homes for sale, each house that pops on the market in your area runs the risk of pulling buyer attention away from yours. For example, if your neighbor gets in on the action and lists their house too, it means you’ll have competition right next door. You don’t want buyers to tour your house and fall in love with someone else’s. You want yours to be in the spotlight. A great agent can make that happen. They’ll help you get your house ready to list, draw attention to everything today’s buyers are looking for, and help you price it right. That way buyers are really drawn to your listing and eager to make it their home. If you’re ready and able to sell now, here’s your chance to get the best of both worlds. Since the supply of homes for sale is growing, you’ll have more options for your own move. But you’ll also be able to sell while your house will still stand out. Bottom LineEven though inventory is still low, you don’t want to wait for more competition to pop up in your neighborhood. Let’s connect to go over the perks of selling before more homes come to the market.  Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place. 1. Home Values Typically Go Up Over TimeThere’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):  Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn't follow the normal pattern, but generally, home values kept rising. This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institute says: “Homeownership is critical for wealth building and financial stability.” 2. Rent Keeps Rising in the Long RunHere’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):  So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you've got a decision to make. Do you want to invest in yourself or keep paying your landlord? When you own your home, you're investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good. As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says: “If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”Bottom LineIf you're tired of your rent going up and want to explore the many benefits of homeownership, let’s talk to explore your options.  Tips for Younger Homebuyers: How To Make Your Dream a Reality

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you. While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side. Here are some helpful tips you may get from a pro. 1. Explore Your Options for a Down PaymentIf a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree. And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones. 2. Live with Loved Ones To Boost Your SavingsAnother thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrate explains: “. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.” 3. Cast a Broad Net for Your SearchWhen you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options. For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains: “Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.” 4. Take a Close Look at Your Wants and NeedsAnd lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says: “An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line. Bottom LineReal estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says, with that support you can make it happen: “The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.” Let’s connect to get you set up for long-term success. |

Let's ConnectWith the correct person by your side, the buying and selling process doesn't have to be full of stress, doubt and anxiety - it can actually be FUN! Archives

July 2024

Categories

All

Jacquelyn Duke, Realtor®

Licensed to Sell in the State of Iowa [email protected] (515) 240-7483 Realty One Group Impact 617 SW 3rd Street Ste 101 Ankeny, IA 50023 Disclaimer: The material on this site is solely for informational purposes. No warranties or representations have been made.

|

RSS Feed

RSS Feed